Pilot study – Swedish companies’ compliance costs for handling VAT legislation

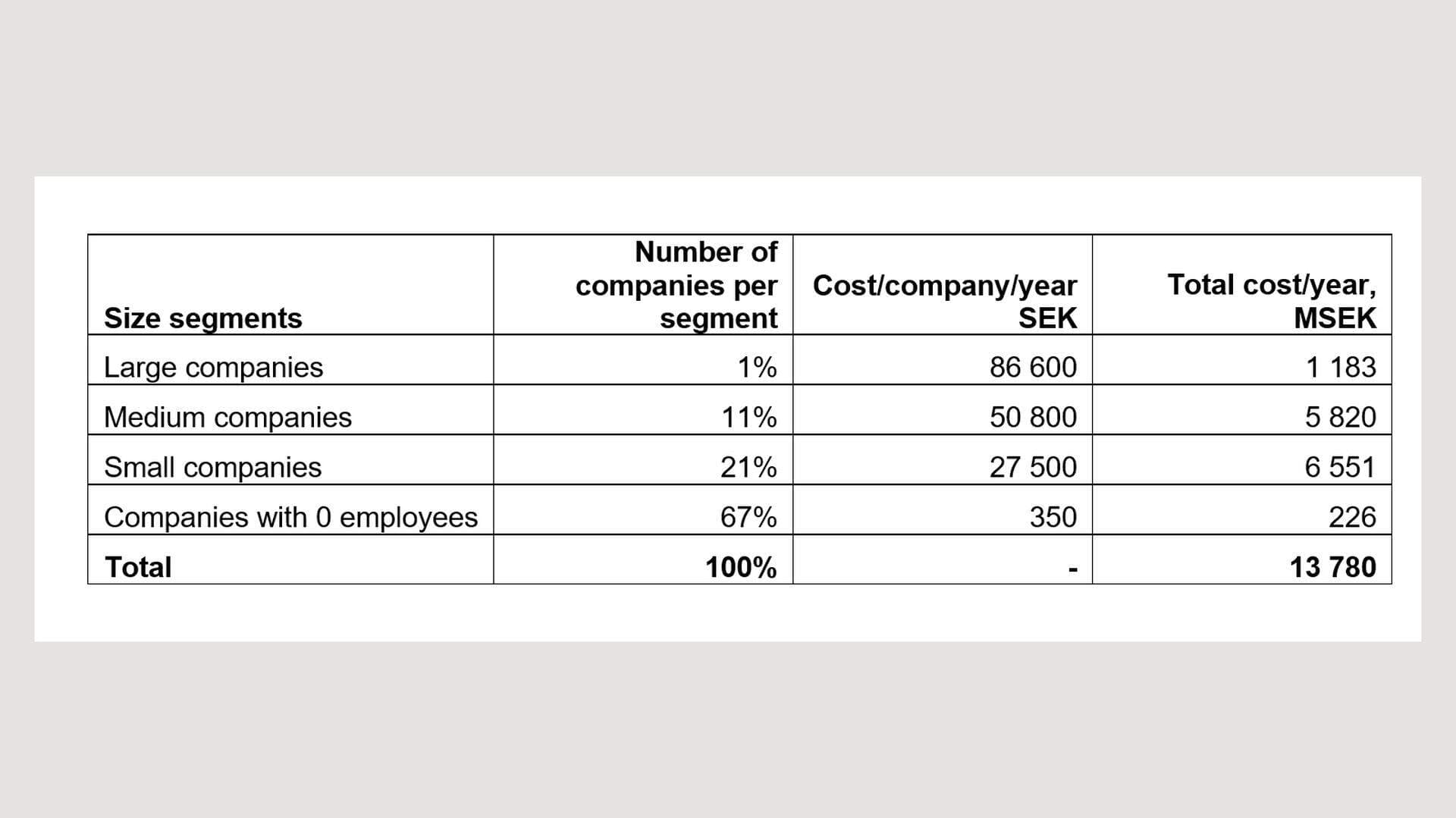

In the spring of 2023, the Confederation of Swedish Enterprise conducted a study to estimate companies’ administrative costs related to Swedish VAT legislation. The calculated indicative administrative cost at the national level amounts to SEK 13.8 billion (Euro 1.2 billion) and affect roughly one million VAT registered companies.

Small companies (1-4 employees) account for about 47% of the total cost. In comparison with calculations made in 2004-05 by Nutek/Tillväxtverket (The Swedish Business Development Agency), costs are estimated to have increased by approximately 25%. The requirement considered to be the most complex and time-consuming is the determination of the input VAT, which accounts for approximately 70% of the total costs.

VAT administration costs Swedish companies SEK 14 billion (Euro 1,2 billion) annually

The study is based on an internationally established method called the Standard Cost Model (SCM). In short, the methodology involves conducting a number of interviews to determine processes and time estimates for companies’ administrative handling of different parts of the legislation. To ensure the methodology, Svenskt Näringsliv decided to initially conduct a partial study, which therefore covers only certain parts of the legislation, primarily the handling of domestic VAT.

The administrative costs have been supplemented with an estimate of primarily material costs. In the study, a couple of typical cases are reported to give an example of the size of educational costs, IT costs, and non-recurring costs linked to the management of the VAT legislation.

Within the framework of the study, a number of observations have been made regarding the functioning of the legislation:

A large part of the interviewed companies waive VAT deductions for representation and handling of leasing cars. The cost of internal resources is often deemed to be greater than the partial VAT deduction that can be made.

Companies that manage composed package solutions state (e.g. hotels) that it is difficult to determine whether the tax base should form a whole or be divided when VAT is to be applied. The assessment is often done differently between companies in the same sector, thus risking competitive disadvantages.

Real estate companies state that they cannot rent premises to companies or organizations not subject to VAT, as this would involve extensive work to ”reverse” previous VAT decisions and deductions with the risk of increased VAT costs.

The digital solutions of the Swedish Tax Authority (SKV) for submitting tax returns, etc., generally receive a good rating. However, several companies state that SKV does not always understand the often quite far-reaching consequences of development and other costs due to changes or reinterpretation of regulations or adjustments of technical solutions.